Why on earth would sophisticated investors choose to lock up their money for a decade or more?

It’s a fair question.

One that baffles many people who first encounter the world of private markets.

In an age obsessed with daily liquidity and instant gratification, it almost sounds medieval to tie up capital for years, unable to sell at the click of a mouse.

Yet some of the world’s largest, most sophisticated investors (pension funds, endowments, sovereign wealth funds) are clamoring for the privilege.

Welcome to the allure of illiquidity.

Private Equity and Private Debt are at the heart of this phenomenon.

And for CFA candidates and finance professionals alike, understanding these asset classes is no longer optional.

The CFA Level III curriculum has recognized the explosive growth of private markets by expanding its coverage through the Private Markets Pathway.

But beyond exam success, this is a topic deeply intertwined with the future of asset management, investment strategy, and even capital formation itself.

Let’s go beyond the textbook and unravel why private equity and private debt are so seductive…

… and why they remain controversial, complex, and career-critical.

The Role of Private Markets in the CFA Curriculum

Private markets used to be a footnote in traditional finance education.

Not anymore.

In CFA Level III, the Private Markets Pathway dives into the structures, cash flow patterns, valuation complexities, and risk-return profiles of private equity and private debt. The emphasis reflects a seismic shift in institutional portfolios.

Why does it matter for CFA candidates? Because the world of investing has changed.

Investors can’t afford to remain exclusively in public markets if they want to hit return targets in a low-rate, highly competitive environment.

Understanding private equity and private debt isn’t just curriculum trivia anymore… it’s essential knowledge for professionals in asset management, consulting, private banking, family offices, and increasingly, corporate finance.

The Case for Private Equity | Buying Control and Engineering Value

Let’s start with private equity – perhaps the better known of the two.

This is the playground of leveraged buyouts (LBOs), growth equity, and venture capital.

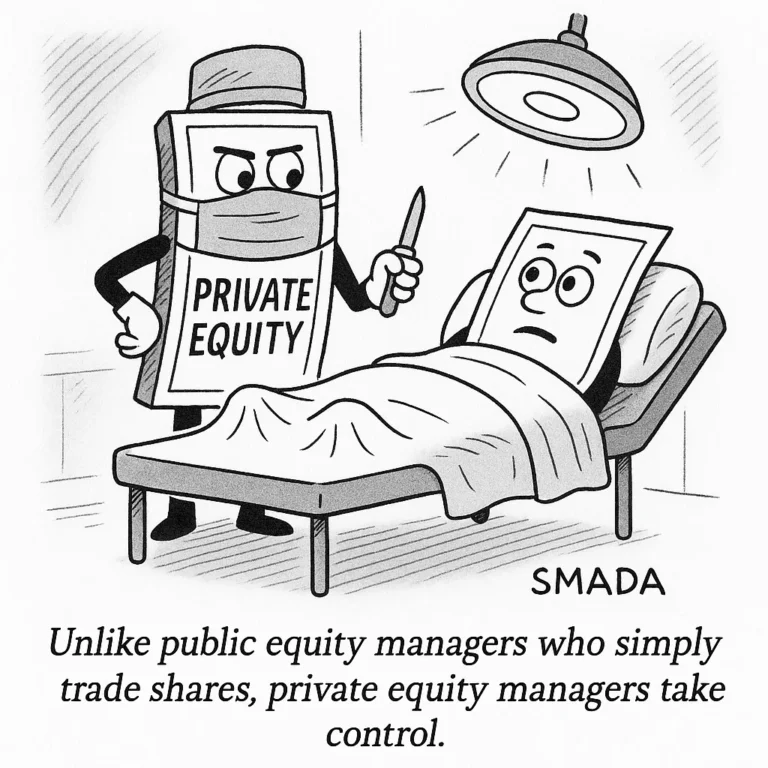

At its core, private equity is about buying businesses, improving them, and selling them later at a profit. Unlike public equity managers who simply trade shares, private equity managers take control. They change management teams, reshape strategies, cut costs, sell assets, expand into new markets, or even bolt on acquisitions.

Consider the case of Hilton Hotels. In 2007, Blackstone bought Hilton for $26 billion in one of the largest LBOs ever. The timing seemed catastrophic – the global financial crisis soon cratered the hospitality sector. Yet Blackstone doubled down on operational improvements and expanded Hilton’s footprint aggressively overseas. When Hilton went public again in 2013, it became one of the most profitable private equity turnarounds in history. Blackstone ultimately earned an estimated $14 billion in profit from the deal.

That’s the power of active ownership.

Private equity funds hunt for alpha >>> returns generated not merely from market movements but from hands-on value creation.

Of course, the recipe isn’t without risk.

Deals are often heavily leveraged, and a poorly timed recession can quickly obliterate equity value. Moreover, the high fees (typically 2% management fees and 20% carried interest) spark constant debate over whether private equity justifies its cost.

The Private Debt Boom

If private equity is about buying and transforming businesses, private debt is about lending money outside traditional banking channels.

Private debt (AKA Private credit) funds emerged in force after the Global Financial Crisis when banks pulled back from lending to smaller and mid-sized companies due to stricter regulations.

Enter private lenders (asset managers, credit funds, insurance companies) eager to step in and provide loans at attractive yields.

These loans can take many forms:

➤ Senior secured loans

➤ Mezzanine debt

➤ Unitranche structures (a single tranche blending senior and junior features)

➤ Distressed debt, and

➤ Special situations.

Imagine a middle-market company seeking $200 million to acquire a competitor. A bank might balk at the leverage ratio or the borrower’s limited collateral. A private debt fund, however, might seize the opportunity to lend at higher yields, negotiate tighter covenants, and earn equity kickers (such as warrants) to sweeten returns.

Private debt became especially appealing during the low-yield years of the 2010s. Institutional investors (starved for income) piled in, enticed by yields of 7-10% compared to paltry returns in public fixed income.

But, like most things, there’s a dark side too.

Private debt is illiquid and opaque.

Pricing is not transparent.

In a downturn, default rates can spike, and recovery values are uncertain.

Critics warn that the surge in private credit has led to lower underwriting standards and hidden risks lurking beneath the surface.

The Illiquidity Premium

So why do investors voluntarily sacrifice liquidity?

The magic phrase is illiquidity premium.

The theory goes like this…

If you’re willing to tie up capital for years, you should be compensated with higher returns. Right?

But here’s the controversy – does the premium really exist after fees and risks?

Empirical research is mixed.

Some private markets asset consultants have research which shows that top-quartile private equity funds have historically outperformed public markets by a wide margin. Yet average or bottom-quartile funds often underperform public benchmarks. Sometimes dramatically.

The same is true in private debt. Investors who pick strong managers may earn attractive risk-adjusted returns. But in the scramble for yield, weaker deals and over-leveraged companies could spell trouble if the economy sours.

The result? Private markets demand exceptional manager selection. Unlike public equity, where low-cost indexing works beautifully, private markets are not “beta” investments.

You’re paying for skill, relationships, and deal sourcing.

Private Markets | The Institutional Gold Rush

Institutional investors have been pouring billions into private markets.

Why?

First, public markets have shrunk. Fewer companies are going public, and many prefer to stay private longer to avoid regulatory scrutiny and market volatility. Private equity fills this financing gap.

Second, institutions need returns. Pension funds and endowments face obligations that traditional stocks and bonds may not cover in a low-return environment. Private markets promise higher returns… and diversification benefits.

Finally, large investors have the scale and patience to commit capital for a decade. Illiquidity is less frightening for a sovereign wealth fund managing multi-generational assets than for an individual needing daily liquidity.

Yet there’s a concern that private markets are becoming victims of their own success.

With so much capital flooding in, valuations have soared, potentially compressing future returns.

Deals are getting bigger and sometimes riskier as managers scramble to deploy capital.

Controversies and Critiques | The Darker Side of Private Markets

Private markets are not without detractors.

Transparency remains a major concern. Investors often rely on self-reported valuations from fund managers, creating potential conflicts of interest.

Critics argue that ‘mark-to-model’ valuations obscure true performance and mask losses during downturns.

Fees are another lightning rod. Critics question whether 2-and-20 fees are justified given that not all funds consistently outperform public markets.

Moreover, private markets face scrutiny over their societal impact. Private equity has been accused of ‘strip and flip’ tactics… acquiring companies, slashing costs, cutting jobs, and exiting quickly.

While success stories like Hilton exist, failures like Toys “R” Us, where debt-laden ownership contributed to bankruptcy and thousands of layoffs, fuel the perception of private equity as ruthless.

Private Markets & Careers in Finance

So what does all this mean for your career?

Private equity and private debt knowledge & skills is now a hot commodity across multiple finance roles.

Asset Management – Institutional portfolio managers increasingly allocate to private markets. Understanding how to evaluate private funds is crucial.

Private Banking & Wealth Management – High-net-worth individuals are gaining access to private market products through feeder funds and semi-liquid vehicles. Advisors must explain complex structures and illiquidity risks.

Investment Consulting – Consultants guide institutions in constructing private market portfolios and selecting managers.

Corporate Finance: Professionals on the corporate side engage with private equity or private lenders during M&A transactions, recapitalizations, or growth financings.

Knowing this topic makes you credible in interviews, especially for roles touching alternatives, institutional sales, or portfolio construction.

Prepare and be ready to discuss…

- The illiquidity premium debate

- How cash flows in private equity funds differ from traditional investments

- The risks in private credit underwriting

- Fee structures and alignment of interests between managers and investors

- Real examples of high-profile deals, both successful and disastrous

If you want to sound sharp in a professional setting, avoid blanket statements like “private equity always outperforms”.

Acknowledge nuances – manager selection, vintage-year effects, fee drag, and market cycles.

Tips for CFA Candidates | Mastering Private Markets

For the CFA exam, private markets can feel overwhelming.

Some tips…

Understand Cash Flow Mechanics.

Learn how private equity funds call and distribute capital. Know the J-curve effect, where returns start negative due to fees and investment costs but improve as exits occur.

Know Valuation Methods.

Be familiar with valuation approaches for private companies (DCF, comparables, precedent transactions) and the unique issues around illiquid holdings.

Remember Key Terminology.

Terms like ‘preferred return’, ‘carried interest’, ‘capital call’, ‘distribution waterfall’, and ‘unitranche’ need to be added to your vocabulary.

Think Conceptually.

Instead of rote memorization, focus on why investors choose private markets and how risks differ from public investments.

Connect Topics.

Private markets tie closely to readings on alternative investments, portfolio management, risk management, and behavioral biases (like overconfidence in manager selection). Make these mental connections.

Common mistakes? Candidates often underestimate the time needed to absorb the many moving parts in these readings (like cash flow timing and fee structures). Don’t skip practice questions in the CFA curriculum’s alternative investments readings.

Resources for Going Deeper

If you’re fascinated and want to dive deeper:

Books

King of Capital (David Carey and John Morris) for a behind-the-scenes look at Blackstone.

Private Debt: Opportunities in Corporate Direct Lending (Stephen Nesbitt) offers insight into private credit.

Reports

Cambridge Associates and PitchBook publish excellent private market research.

Podcasts

Dry Powder (Bain & Company) and Private Equity Fast Pitch (Northstar) are great resources for hearing practitioners discuss real-world challenges.

News Sources

PE Hub, Private Equity International, and Private Debt Investor offer timely deal news and trends.

A Final Word | Digging Below the Surface

Private markets are seductive because they promise something rare:… the chance to earn outsized returns by investing where others can’t (or won’t) go.

But beneath the glossy brochures and billion-dollar deal headlines lie significant risks, complexities, and controversies.

For CFA candidates and finance professionals, understanding private equity and private debt has moved beyond simply passing an exam. It’s about grasping how modern capital markets work – and how capital shapes businesses, jobs, and entire economies.

Stay curious. Keep questioning. And remember that in finance, the real alpha often comes from knowing what lies beyond the obvious.